“Calm wealth management”: how to stay the course through volatility

When markets move, the question isn’t whether your portfolio can handle it. It’s whether your plan was designed to.

You have accounts across more than one bank. You've invested across asset classes: equities, bonds, perhaps some property, a structured product or two over the years. Decisions made at different moments, with different advisers, for different reasons. Some have done well. On balance, you're in a reasonable position.

When markets drop — really drop, not a blip but a sustained, headline-generating correction — you open multiple apps, look at different numbers in different places, and try to construct a picture that no single view gives you. No single institution holds the whole thing. No single document shows you what it all adds up to, what it's exposed to, or where it's taking you.

The temptation is to act — to do something. It's a reasonable instinct. It is also one of the most reliably costly ones in wealth management.

What we believe at Life First Advisory:

Calm is not a temperament. It is what a well-built plan produces — one that was designed for volatility before it arrived, not in response to it.

The problem with a collection of good decisions

There is a financial profile more common than the industry tends to acknowledge. The person who has done everything broadly right — diversified across banks, accumulated across asset classes, responded sensibly to opportunities as they arose — but who has never had a single, integrated view of what it all adds up to.

The multi-banked, multi-asset investor typically has strong individual positions and a fragmented overall picture. Each product was chosen for a reason. Each bank relationship has some logic. The portfolio, in aggregate, was never designed as a portfolio. It assembled itself.

This matters more as retirement approaches — and significantly more once income is being drawn from it. In accumulation, fragmentation is mainly an efficiency problem. In decumulation, it becomes a sequencing problem. Sequencing errors in retirement are expensive and often irreversible.

When we sit with someone in this position, the first task is never to change anything. It is to construct the view that doesn't yet exist: what is actually here, what is it doing, what is it exposed to, and how does any of it connect to the income this person needs their wealth to produce. Only once that picture exists can we assess whether anything needs to change — and whether what feels like volatility risk is actually volatility risk, or simply the disorientation of never having seen everything in one place.

What volatility actually tests

A market correction is not primarily a financial event. It is a diagnostic one.

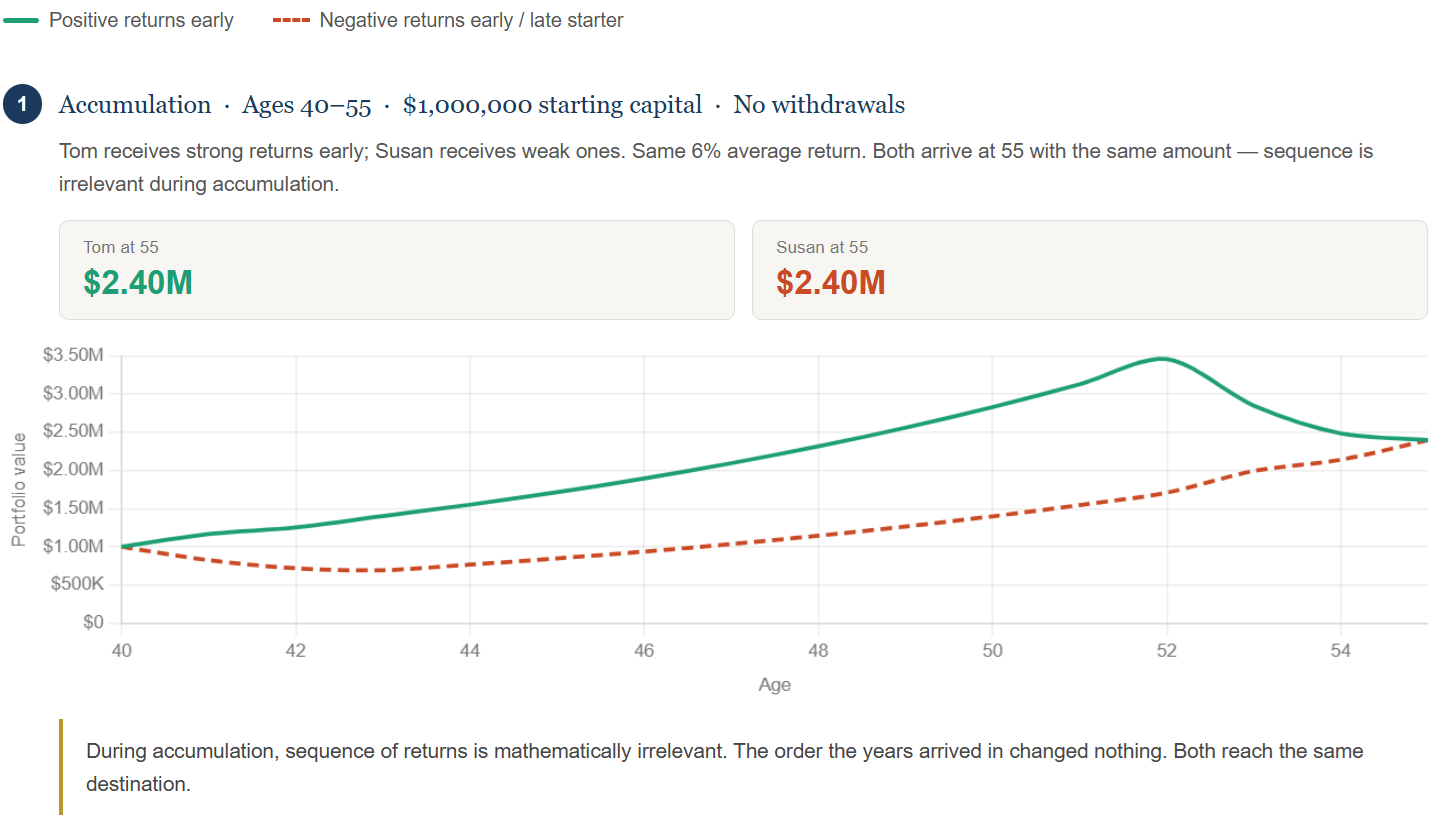

Consider two investors — Tom and Susan. Both invest $1,000,000 at age 40 and achieve the same average return of 6% per annum after fees over fifteen years. Tom receives strong returns early; Susan receives weak ones. By age 55, both arrive at exactly the same amount.

Decumulation is an entirely different proposition. John and Sarah, both 55, each start with $3,000,000 and withdraw $120,000 in year one, with annual increments of 2% — the same 6% return, the same withdrawal behaviour. John receives strong returns early. Sarah receives weak ones.

Sarah's portfolio depletes. John's does not. Every variable is identical. The sequence alone changed the outcome.

This is what a correction tests in practice. For the pre-retiree — still accumulating, perhaps five to ten years from drawing income — a correction asks whether the plan accounts for poor returns arriving in the years immediately before retirement. A significant drawdown at that moment, if the portfolio isn't structured for it, can permanently reduce the income that wealth is capable of producing. Not because the market doesn't recover, but because the recovery happens after withdrawals have already begun at depressed prices.

For the retiree already in drawdown, the stakes are more immediate. Spending from a declining portfolio means selling assets at lower prices to fund a life that hasn't changed in cost. A portfolio that sustains forty-four years of withdrawals under normal conditions may not sustain the same withdrawals through a correction in its early years — and forty-four years is not a conservative estimate. For a couple retiring at fifty-five in Singapore today, one partner living into their late nineties is a planning assumption, not an outlier. Factor in legacy intent — wealth meant to pass to children or to causes — and the time horizon extends further still.

What volatility reveals is not whether markets are behaving unusually — they are not — but whether the plan was built for the world as it actually is.

Why starting early is the most structural decision you can make

The scenarios above share one assumption: both investors begin at the same moment. In practice, the more consequential question is not how you manage volatility but how much time your money had before you started drawing from it.

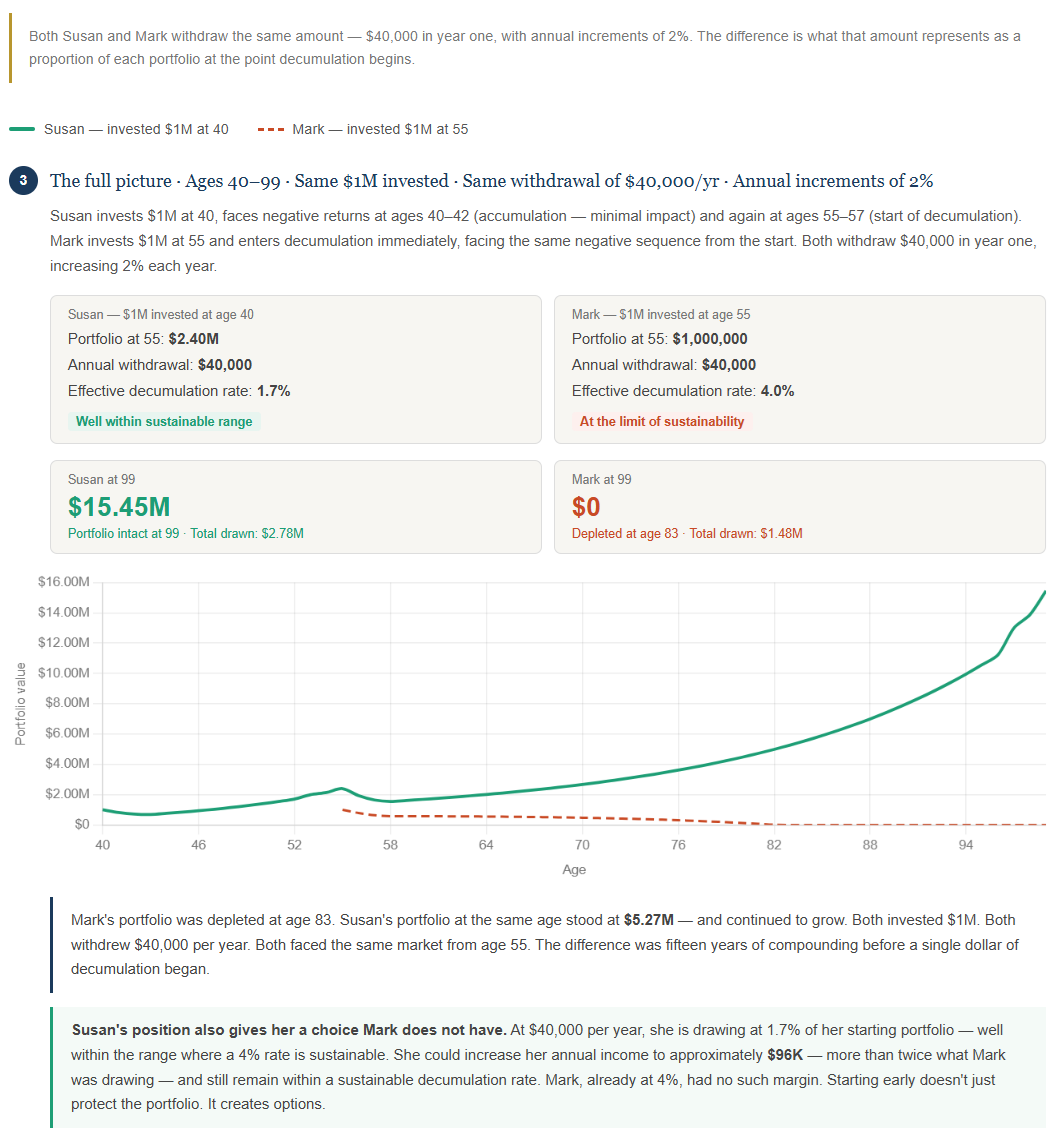

Susan's full story makes this clear. She invests $1,000,000 at age 40, faces bad markets in the early years, and faces them again at the start of the decumulation phase at fifty-five. The bad markets during accumulation changed almost nothing — as the first scenario shows, sequence doesn't matter when no money is leaving. She arrives at fifty-five with approximately $2.4 million, and begins drawing $40,000 per year with annual increments of 2%.

Mark invests the same $1,000,000 — but not until age 55. He enters decumulation immediately: the same $40,000 per year, the same annual increments, the same market Susan faces from fifty-five.

The withdrawal amount is identical. What is not identical is what it represents. Susan's $40,000 per year is approximately 1.7% of her portfolio at the start of decumulation — well within the range a 6% return can sustain indefinitely. Mark's $40,000 is 4% of his — at the limit of what the same return can sustain when markets begin poorly. Same dollar leaving each account. Entirely different structural positions.

Mark's portfolio depletes. Susan's does not — and she has a choice Mark never had. At any point, she could increase her annual income to approximately $96,000 — more than twice what Mark was drawing — and still remain within a sustainable decumulation rate. Starting early doesn't just protect the portfolio. It creates options.

This is what starting early actually means. Not discipline for its own sake — architecture that determines both the resilience and the range of the decades ahead.

The withdrawal you didn't plan for

Market volatility is the sequence risk most investors can see. There is another — less visible, more likely, and rarely planned for.

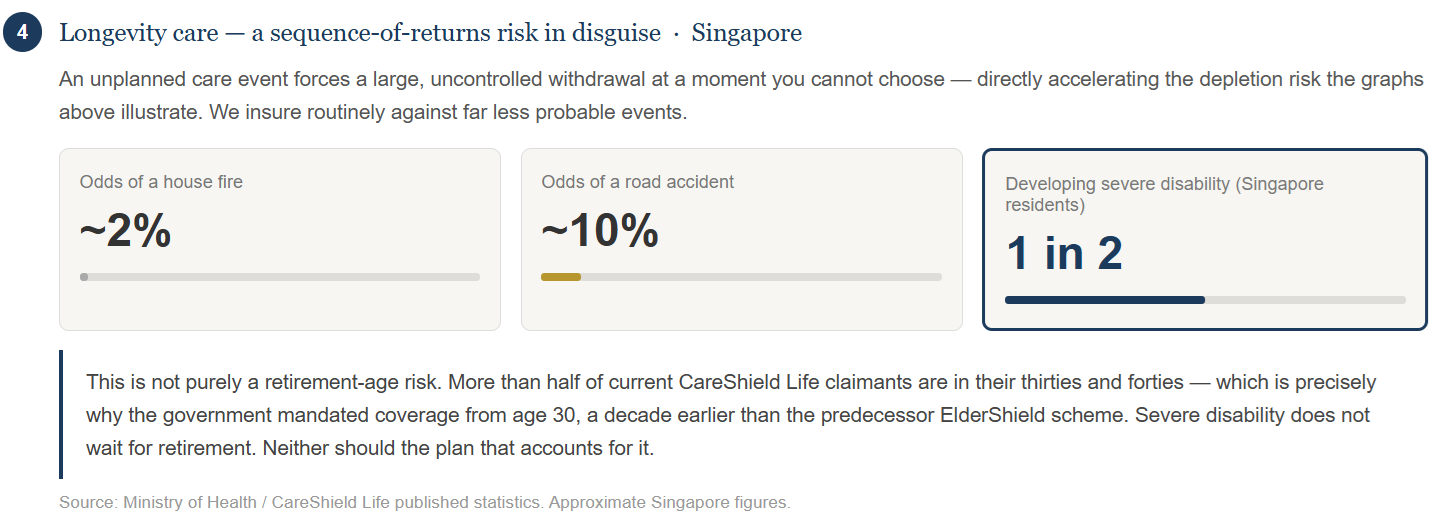

A long-term care event does not announce itself. It arrives as a stroke, a fall, the slow progression of dementia, or the moment when someone who has always managed alone simply cannot any longer. And when it does, it forces something that most portfolio analyses never model: a large, sudden, uncontrolled withdrawal at a moment you cannot choose — the kind of unplanned depletion the graphs above illustrate.

The Ministry of Health estimates that one in two Singapore residents will develop severe disability at some point in their lifetime. More telling for anyone reading this in their forties or fifties: more than half of current CareShield Life claimants are in their thirties and forties. The government moved the mandatory coverage age from forty to thirty — a decade earlier than the predecessor ElderShield scheme — because the data was clear. Severe disability does not wait for retirement. It can arrive well before it.

An unplanned care event does not simply cost money. It disrupts the sequencing of everything: which assets are liquidated, in what order, at what price, and at what point in the decumulation timeline. A portfolio structured for a thirty-year income horizon was not designed to absorb a sudden, sustained six-figure expenditure in year three of decumulation. The plan that appeared robust under market stress may not be robust under this kind of stress.

This is not an argument for any particular product. It is an observation that managing longevity care risk is part of managing sequence risk — and that a plan which has not addressed the former has not fully addressed the latter.

How a structured plan holds through a downturn

We design income plans around one principle: no single part of the plan should have to do everything at once.

In accumulation, this means the assets closest to retirement do not carry the same risk profile as those intended to grow over a fifteen-year horizon. Capital needed to fund income in five years should not be fully exposed to equity volatility. Capital that won't be touched for fifteen years can be — and should be.

In decumulation, the same logic extends across time. We work with a time-segmented structure: near-term income needs held in lower-volatility assets, funded without selling growth positions during a correction; a medium-term reserve positioned to replenish that near-term layer as it deploys; long-term growth assets left to recover and compound without pressure. For clients with legacy intent, that long-term layer carries a second purpose — it is not only funding their later decades, it is the capital most likely to transfer. Protecting its compounding runway is not a luxury. It is the plan.

What this structure produces — and what no amount of willpower produces in its absence — is a portfolio where the rational response to a downturn genuinely is to hold. Not because holding feels brave. Because the plan already accounts for the downturn, the near-term needs are funded, and there is nothing that urgently needs to be done.

That is what calm wealth management means. Not the absence of emotion but the absence of structural pressure to act.

The coordination question

For the multi-banked investor, the core issue is often not risk. It is visibility.

When assets are held across several institutions without an integrated view, it is genuinely difficult to know whether the overall portfolio is exposed to what you think it is. Positions that appear diversified may, in aggregate, be concentrated in the same sectors or risk factors. Multiple vehicles may be doing the same job at layered cost. Assets notionally allocated to different purposes may never have been formally connected to an income plan or a retirement date.

Coordination compounds, just as capital does. A well-coordinated portfolio of ordinary assets will consistently outperform a fragmented collection of individually strong ones — because it eliminates redundancy, reduces unnecessary cost, and means every position is earning its place in the context of the whole. Bringing that coordination into focus is often the highest-value work we do. It rarely involves dramatic changes. More often, it involves finally seeing what is already there — and making deliberate decisions about what stays, what goes, and what role each piece plays going forward.

On the decision to stay the course

Staying the course through volatility is not passive. It is the most active decision in the plan — the one that requires the most preparation, the most architecture, and the most clarity about where the plan is going.

The investor who holds through a correction because they have a coordinated, time-segmented plan and a clear income picture is making a considered decision based on evidence. The investor who holds because they're hoping it works out is making a different kind of bet. The behaviour looks identical from the outside. The foundations are entirely different.

If the current market is making you uncertain, the right question is not whether to change your allocation. It is whether you have a plan that was designed to handle this — and whether you can see it clearly enough to trust it. If the answer is yes, the correction changes nothing. If the answer is anything less than yes, that is the more important conversation.

We’d welcome a conversation.

If the current climate has surfaced questions about whether your wealth is as coordinated as it could be — across banks, across asset classes, across the full arc of what you're building toward — a discovery meeting with Life First Advisory is a good place to start.

For those carrying a substantial investment portfolio across external institutions, we offer something more specific: a structured, objective second opinion on what you hold, how it's positioned, and where the gaps are. No agenda other than clarity.

Frequently asked questions

If I have a well-diversified portfolio, why does a market correction still feel unsettling?

Diversification addresses risk within a portfolio. It doesn't tell you how the portfolio connects to your income needs, your retirement timeline, or what it's supposed to produce and by when. The unsettled feeling during a correction is usually the absence of that picture, not a problem with the assets themselves. A genuinely structured plan removes the uncertainty that diversification alone cannot.

The graphs show one portfolio depleting. Does that mean I should reduce equity exposure in retirement?

No — and blanket de-risking is one of the more expensive habits in retirement planning. The answer to sequence risk is structure, not asset elimination. Time-segmented planning means near-term income needs are funded from lower-volatility assets, so growth positions are never sold under pressure. Removing equities removes the engine that sustains a thirty-to-forty-year decumulation.

I'm already in the decumulation phase. What should I do during a correction?

If your plan was built with a time-segmented structure, the answer is nothing. The near-term income layer was designed for exactly this — so that growth assets are never sold under pressure. If you are drawing directly from an undifferentiated portfolio, a correction is genuinely more disruptive. The conversation worth having is how to restructure before the next one, not how to react to this one.

The comparison between Susan and Mark involves very different portfolio sizes at 55. How does this apply to my situation?

The relevant variable isn't the dollar figure — it's the relationship between what you have at the start of decumulation and what you need to draw each year. Susan and Mark both invested $1,000,000 and withdrew at the same 4% rate. The difference was time. Fifteen additional years of compounding before decumulation began gave Susan a portfolio large enough to absorb a poor opening sequence that depleted Mark's. Wherever you are in that arc, the principle holds: the more time your capital has to compound before withdrawals begin, the more structural resilience you carry into retirement.

What does long-term care have to do with my investment plan?

More than most people expect. A care event forces a large, unplanned withdrawal at a moment you cannot choose — often at precisely the wrong point in the market cycle. It doesn't just cost money. It disrupts the sequencing of which assets get sold, in what order, and at what price — the same dynamics that deplete portfolios in the decumulation scenario above. A plan stress-tested for market volatility but not for a sudden, sustained care draw has not been fully stress-tested. We address longevity care risk as part of income planning, not as a separate conversation.

My assets are spread across several banks. Does that protect me or create risk?

Both, potentially — but the more important question is whether anyone has a complete, integrated view of what you own and whether it is working together. Multi-banking can reduce counterparty concentration and preserve optionality. It can also produce duplication, layered cost, and a fragmented picture that makes coherent planning difficult. The number of institutions is not the issue. The absence of a coordinating view is.

What does a second opinion from Life First Advisory actually involve?

We review the complete picture of what you hold externally — across banks, asset classes, and structures — and provide a clear, objective assessment of how it's positioned, what it's costing, where the gaps are, and how well it connects to your income and legacy goals. It is a structured analysis, not a sales conversation. We believe it is one of the most useful things an investor with a substantial external portfolio can do — regardless of whether they choose to work with us afterward.